An exciting first step in a broader tokenized vaults offerings

Like people of good taste everywhere, you have probably already heard about Synthetix’ refreshed strategic vision, and about one of its key pillars: graduating from being a B2B financial infrastructure protocol to also designing and curating a set of vaults and tokenized strategies. These strategies will provide a user-friendly, composable, highly-abstracted way for new users to interact with Synthetix.

Following the acquisition of TLX, Synthetix is working on launching a suite of Leveraged Tokens on both Optimism and Base networks. So, what are leveraged tokens?

What are leveraged tokens?

Simply put, leveraged tokens are the tokenized representation of an ownership position in a levered strategy: aiming to earn multiple times the price movement of an underlying asset, like ETH or BTC. So, an ‘ETH3x’ long token aims to go up and down three times as fast as ETH.

Their main value proposition is short-term convenience: compared to managing a levered position yourself using derivatives or money-market looping, a leveraged token offers transferability, fungibility, composability, and automatic protection from liquidation. Wouldn’t it be nice to just see your levered position in your wallet next to your ETH and your memecoins?

Structured products that give levered exposure to a base asset have been around forever and are a thing in Tradfi. A notable example is a $25bn 3x Nasdaq ETF, which ‘seeks daily investment results, before fees and expenses, that correspond to three times (3x) the daily performance of the Nasdaq-100 Index’.

In centralized crypto, FTX and Binance both used to offer them, and other DeFi actors currently offer them. So they are a thing, and we hope to make them a bigger and better thing.

A taxonomy of leveraged tokens

Despite being such a simple financial instrument, the design space for leveraged tokens is practically infinite. Principle characteristics to look out for include:

- Underlying asset and leverage level: What return are we trying to emulate? BTC3X? DOGE5X?

- Source of leverage: How is the underlying levered position achieved? Using a derivative position on a Perp DEX like Synthetix? Buying spot tokens on margin using a spot DEX like Uniswap and a lending market like Aave?

- Rebalancing mechanics: As the price of the underlying moves around and leverage strays from its 3x target, how does the strategy do its incremental trading (‘rebalancing’) to get back to target? Is it programmatic or discretionary? Performed at fixed time intervals or when a leverage limit is reached? Is it trust-minimized and encoded in the contract logic, or performed by a trusted off-chain actor?

- Mint/redeem experience: Upon buying a fresh token and selling it back to the pool, are any timelocks or size limitations enforced? What fees are charged? Are the trading costs that a new or departing investor might cause because he will trigger a rebalance incurred by the investor or the collective token holders?

Financial Performance

There is an unavoidable tracking error between the returns of the underlying instrument, multiplied by the leverage factor, and the returns of the strategy underpinning the leveraged token. This error stems from four places:

- Fees: Management fees, mint, and redemption fees charged by the vault.

- The cost of carry: Where there is leverage, there is a loan. Someone is lending us capital so we can have more exposure to the underlying asset than just buying it outright. In practice, the cost that will be borne is either the stablecoin borrow rate if the leverage is achieved by borrowing (e.g., USDC on Aave) or the perpetual contract funding rate if it is achieved by opening a long position on a derivatives DEX like Synthetix.

- Trading costs: The underlying vault needs to trade constantly. Mints, redemptions, and movements in the price of the underlying asset all cause the effective leverage to deviate from the target. When the vault trades, it will incur:

- Trading fees: like the swap fee on Uniswap or the maker/taker and keeper fees on Synthetix.

- Slippage: trading at a price that is different from the real fair value at that time. Careful mechanism design is needed: the predictable, deterministic nature of the vault’s trading pattern make it vulnerable to front-running (e.g., buying ahead of the vault and selling behind it). In Tradfi there is a whole industry trying to trade ahead of lumbering giants like SPY ($600bn+) and QQQ ($300bn+).

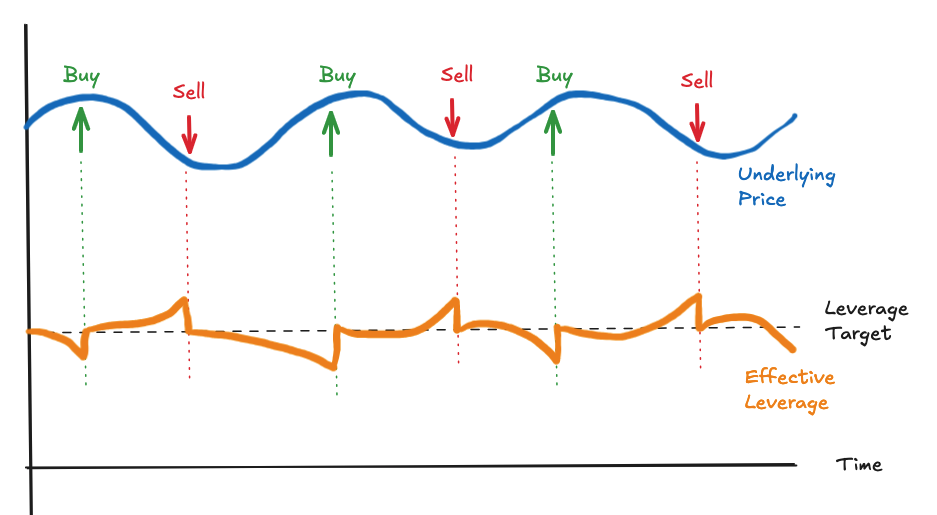

- Volatility decay: The least intuitive one. This refers to the tendency of levered products to underperform their target due to the volatility in the underlying instrument. In a range-bound market that trades up and down with little overall directional trend, the vault will tend to ‘buy high’ (price goes up, leverage goes down, time to buy) and sell low (price goes down, leverage goes up, time to buy):

The above sounds unpleasant, but it’s the necessary price to pay for in-built liquidation protection, which is a great feature: if we are levered long and the price starts going down, the vault will start selling so we can stay in the fight and not go broke.

For very volatile products like crypto, it makes sense to carefully study acceptable leverage bands that let us faithfully track the underlying while minimizing trading costs and volatility decay.

Conclusion

As you can see, the best of Synthetix’s storied DeFi pedigree has been brought to bear on the surprisingly deep question of how to build a leveraged token. A carefully designed product will:

- Offer the discerning DeFi user a convenient, safe, one-click way to gain a levered exposure that is fungible, transferrable (can be sold or gifted to a friend), and composable (can be used in DeFi as collateral to borrow against and more).

- Target a leverage level that is exciting, mindful of the tracking error described above. This error means these tokens are best used as short or medium-term ways to get a lot of price exposure.

- Carefully think about fees, leverage management, and the underlying Defi protocols at play to achieve its financial objectives in a way that is safe, fair, and transparent.

You can experience Synthetix Leveraged Tokens now on leverage.synthetix.io – but stay tuned, we’ll be releasing V3 Leveraged Tokens on Base shortly, along with a promotion to celebrate the launch. Be sure to join our new Telegram channel for this and all major Synthetix developments.

To learn more about Synthetix Leveraged Tokens, see our docs.